-

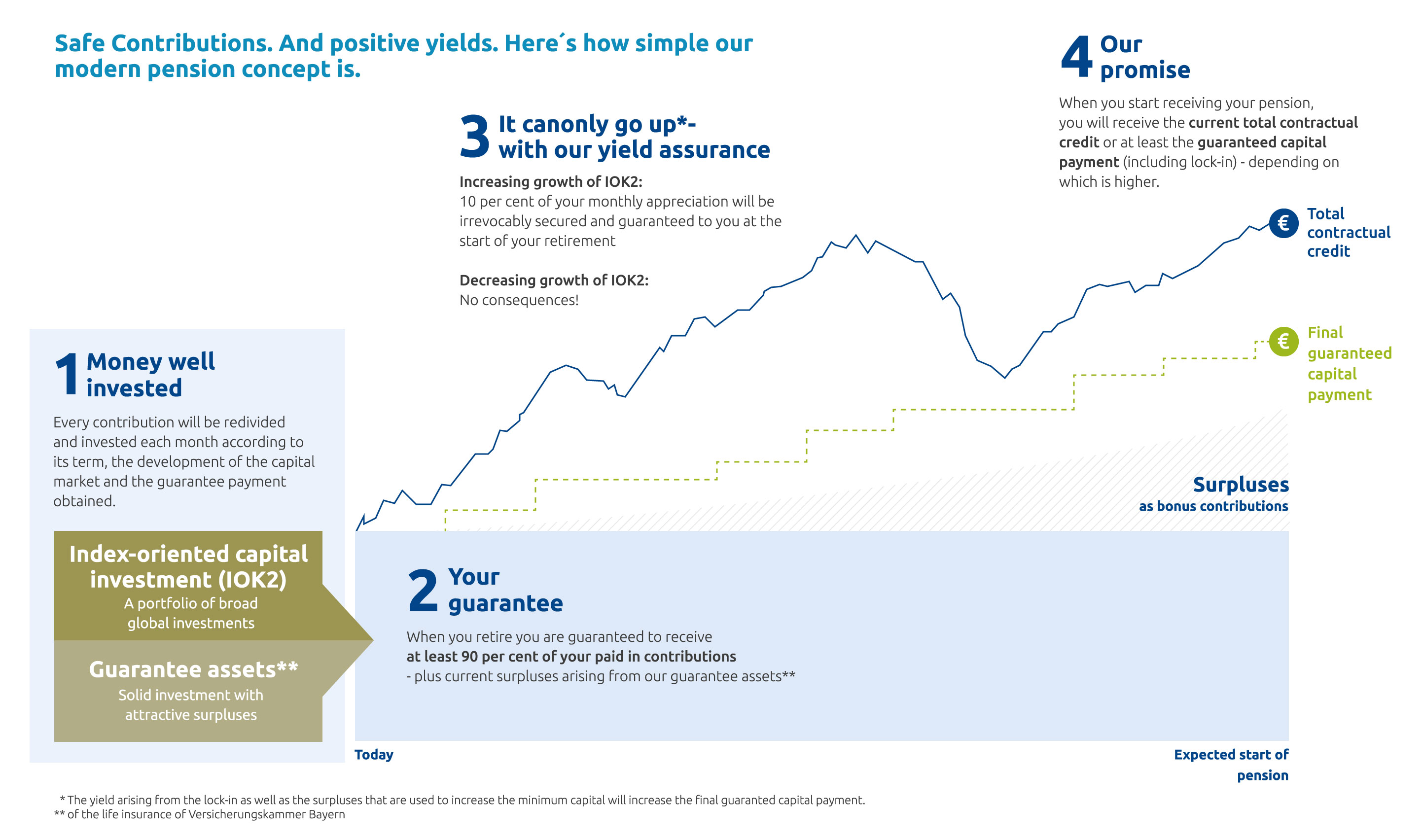

Additional pension with growth guarantee.

A pension plan you can rely on.

- Future-proof investment in euros

- 90% guaranteed payout plus surpluses

- State subsidised

Why more than 10% of the population secures its future with us

Your advantage

- lifelong pension

-

-

With life expectancy historically at it´s highest, our lifelong pension is a real asset. Of course you can also choose to get your pension payed out in one payment when you retire.

-

- investment in euros

-

-

The Euro ranks as one of the most important currencies in business today. Therefore it is a solid choice for your pension!

-

- In safe hands with S-Finance Group

-

-

As a part of the S-Finance Group we build on the experience of one of the biggest financial services providers on the market. With a combined business volume of 3,330 billion euros, the S-Finance Group is the largest financial services provider in Europe.

-

- Flexible investment possibilities

-

-

We offer all common pension plans on the icelandic market today. Wether it is "Séreignarparnaður" (Employer funded pension), "Tilgreind séreign" (investing a part of your mandatory pension in WachstumGarant or your private pension plan - we've got you covered!

-

Did you know?

Iceland´s pension system can only cover up to 73% of your current income when you retire.

That’s why people in Iceland start their own additional pension at the age of 28 on average.

- Further product details

-

-

- Minimum contract duration of 12 years.

- Your contributions will be invested in euros with our growth guarantee.

- You can claim contributions against your income tax within the assessment limit.

- The first payout can begin once you reach 60 years of age and you can choose between a lump-sum settlement and/or a monthly pension for the rest of your life.

- Income tax is paid on payouts.

PDF documents for downloading:

-

- Further product details

-

-

- Minimum contract duration of 12 years.

- Your contributions will be invested in euros with our growth guarantee.

- The first payout can begin once you reach 62 years of age, based on the rules of the pension fund you have selected.

- Income tax is paid on payouts.

PDF documents for downloading:

-

- Further product details

-

-

- Minimum contract duration of 12 years.

- Your contributions will be invested in euros with our growth guarantee.

- Pension insurance that you pay directly (after tax).

- When the contract comes to an end (starting from when you reach 62), you can choose between a one-time payment and/or a lifelong monthly pension.

- When the contract comes to an end, capital gains tax will be paid on the yields.

PDF documents for downloading:

-

- Further product details

-

-

- Minimum contract duration of 12 years.

- Your contributions will be invested in euros with our growth guarantee.

- You can claim contributions against your income tax within the assessment limit.

- The first payout can begin once you reach 60 years of age and you can choose between a lump-sum settlement and/or a monthly pension for the rest of your life.

- Income tax is paid on payouts.

PDF documents for downloading:

-

- Further product details

-

-

- Minimum contract duration of 12 years.

- Your contributions will be invested in euros with our growth guarantee.

- The first payout can begin once you reach 62 years of age, based on the rules of the pension fund you have selected.

- Income tax is paid on payouts.

PDF documents for downloading:

-

- Further product details

-

-

- Minimum contract duration of 12 years.

- Your contributions will be invested in euros with our growth guarantee.

- Pension insurance that you pay directly (after tax).

- When the contract comes to an end (starting from when you reach 62), you can choose between a one-time payment and/or a lifelong monthly pension.

- When the contract comes to an end, capital gains tax will be paid on the yields.

PDF documents for downloading:

-

PM-Premium Makler

PM-Premium Makler GmbH

Garðatorgi 7, 210 Garðabær

Garðatorgi 7, 210 Garðabær

Write to us or give us a call!

(Mon. - Fri. 9 am to 12 noon and 1 pm to 4 pm)

(Mon. - Fri. 9 am to 12 noon and 1 pm to 4 pm)

Get more information on PrivatRente WachstumGarant

- Is my pension plan secure even though I’m participating in the capital market?

-

-

- “A lifelong guaranteed pension that can only go up.” What does this mean?

-

-

- Why does it make sense to invest the pension in euros?

-

-

- Are partial capital withdrawals or contribution exemptions possible?

-

-

- What happens to the paid-in contributions in the event of my death?

-

-

More than 200 years of experience you can trust